You may think that all insurances are the same. However, it isn’t, as insurance product contains various benefits and coverage. There is insurance that’s for temporary needs, while some are designed for long-term or lifelong purposes. So, evaluating your financial goals and the risks you want your insurance to cover is essential to consult a licensed insurance agent.

Term life and permanent life are the common types of insurance we hear. But it’s essential to recognize what they offer and why they differ. Initially, individuals should be able to identify their needs and financial goals first. In this way, they’ll be able to determine which insurance suits them and their condition best. So, term life or permanent life? Let’s figure out.

What is Term Life vs Permanent Life Insurance?

Term life insurance primarily provides coverage for a specific time or period. The coverage usually lasts for 10, 20, or 30 years. This insurance is also more affordable than permanent life insurance, making it an ideal option for individuals with temporary financial needs.

Meanwhile, permanent life insurance provides lifetime coverage as long as premiums are paid. Its premiums are usually higher. However, they stay consistent throughout the policy. A tax-free death benefit is also paid to beneficiaries after the policyholder’s passing. Moreover, permanent life insurance comes in different forms, such as:

- Whole life

- Universal life and

- Variable life

Take note that these forms come with unique features and investment options. You may choose what suits you best, but it’s highly recommended to discuss this first with a licensed insurance agent to understand them better. It’s also advisable to inquire and review various agencies. Ensure that you gather insights about the insurance products and options they offer.

Term Life vs Permanent Life Benefits

As discussed above, both insurances offer unique benefits. Still, it’s also essential to recognize their downsides for you to be able to weigh the options better. Insurance is an excellent source of financial protection. Still, individuals should consider affordability, duration, coverage, and general benefits. Overall, both insurances can be your best choice.

Term Life Insurance

Term life insurance offers financial security through its affordability and predictable fixed premiums, making it an accessible and budget-friendly option for those with temporary financial needs. This will highlight the key benefits of term life insurance.

Affordability

If you’re the type of person who’s on a budget, term life insurance can be your best option. This insurance is usually known for its accessible nature, making it easier for you to benefit from it. It’s an ideal go-to insurance for your temporary financial needs.

Fixed premiums

The premiums for term life insurance are consistent throughout its term. As a result, it provides the advantage of predictable budgeting. Fixed premiums offer a significant advantage for individuals and families when it comes to making well-informed choices.

Temporary coverage

Suppose you need short-term financial needs such as income replacement, mortgage protection, or funding your child’s education. In that case, term life insurance is a good choice for you. Not everyone is into lifelong benefits or coverage. Some just want a temporary and quick solution. So this one’s for you.

Simple and straightforward

It’s not only affordable, but it’s also straightforward. This insurance focuses solely on death benefits without worrying about cash value or investment elements. When a policyholder passes, the beneficiaries left will still be able to manage themselves financially without too much burden.

Convertible

Suppose you’re thinking of switching to permanent life insurance. In that case, some term policies offer individuals the option to convert to permanent insurance without needing a medical exam. This characteristic suits people dealing with sudden life changes and deciding to go for permanent benefits to manage their lifetime plans.

Customizable terms

Policyholders can enjoy flexibility and adaptability in terms of selecting the duration of their term life insurance coverage. This feature is especially beneficial as it allows people to tailor their insurance plans according to their financial needs, goals, and responsibilities. However, consult a licensed insurance agent for better guidance and learn more about this feature.

Permanent Life Insurance

Permanent life insurance stands out with its lifelong security, offering a range of unique benefits distinguish it from traditional term coverage. This introduces the key advantages of permanent life insurance.

Lifelong coverage

This feature is what permanent life insurance is mainly known for. It’s a good choice if you have lifelong financial plans. Regardless of when death occurs, permanent life insurance guarantees that the tax-free death benefit will be provided to the beneficiaries. It can help cover funeral costs, outstanding debts, and estate taxes and provide adequate financial support to surviving family members.

Cash value accumulation

These policies come with a built-in cash value feature that increases in value over time, which in turn provides financial savings for you. Through this feature, you can easily manage your finances, especially during times of need.

Financial planning

Permanent life insurance plays a vital role in acting as a safety net and a savings account. It can be an effective financial security against various financial crises. Overall, this grants long-term protection to your family and fosters an effective financial plan.

Asset protection

The cash value can be utilized or borrowed from the policyholder while they are alive. It can be used for financial requirements, including emergencies or retirement income. This insurance serves as a valuable tool for long-term financial planning, thus fostering peace of mind. Moreover, a licensed insurance agent can teach you more about asset protection.

Flexible premiums

This feature gives policyholders the freedom to choose to pay more or less than the scheduled premium amount within certain limits. This allows them to pay higher premiums when their finances are strong, which boosts the policy’s cash value and the death benefit’s growth. On the other hand, they can also have the option to go for low premiums to keep the policy active without creating a strain on their finances.

Establish your legacy

When death occurs, our loved ones are subject to financial hardships. However, permanent life insurance provides a tax-free sum of money, which acts as a fund to manage your loved one’s financial needs even after your passing. Additionally, you can also continue supporting your desired charitable organizations by naming the organization as one of the beneficiaries.

Choosing Your Insurance: Term Life Insurance or Permanent Life Insurance?

Before making up your decision, it’s worth noting that both insurances have pros and cons. Evaluating your conditions and financial needs should be the first thing you need to consider. In this way, you’ll be able to determine what you really need according to your plans and responsibilities. While both insurances are beneficial, they serve different purposes.

It’s important for individuals to weigh factors to ensure a smooth sailing experience in insurance. In this way, they’ll be able to recognize the type of insurance they need according to their financial capability and condition. Meanwhile, here’s an overview of the factors to be considered. Take note that investing in insurance is a serious matter. Thus, one should assess oneself first before making a decision on what insurance type to invest in.

Financial goals and needs

First and foremost, individuals should consider and evaluate their financial objectives, such as income replacement, debt coverage, retirement planning, and estate preservation. This is to ensure that individuals will be able to accomplish their financial goals through investing in insurance. Always remember that investing in insurance requires a specific plan in general.

Budget and affordability

One of the most important factors to consider is your capability to spend on insurance. Insurance is definitely not one of the cheapest options, so it’s also essential to take a look at your financial budget. However, its positive sides are undoubtedly rewarding and grant lifelong benefits for you and your loved ones.

Duration of Coverage Required

Another important thing is to consider the length of time you need coverage. Term Life Insurance is ideal for temporary needs, while Permanent Life Insurance provides lifelong benefits and financial protection. We advise you to consult a licensed insurance agent so you are able to decide which insurance fits you best.

Flexibility and Future Planning

Think about the possible changes in your financial situation and ensure that your coverage is flexible enough to align with your financial needs and conditions.

Health and Age

Your health and age can impact your insurance eligibility and premium rates, so it’s essential to consider these factors before making a decision. For instance, if you have a history of heart problems, life or health insurance may benefit you better with favorable terms.

Conclusion

As we all know, both insurances provide quality benefits. However, their coverage and length differ from each other. As mentioned above, the most important thing individuals should do is to thoroughly assess their financial situation, capabilities, and needs. Consider the factors listed above for a seamless insurance experience.

Better yet, you can consult our finest financial advisors or a licensed insurance agent at The Cook Group. We’ll help you make a difference and understand insurance better. We aim to educate individuals about insurance’s whats, hows, and whys. Visit our website for more details.

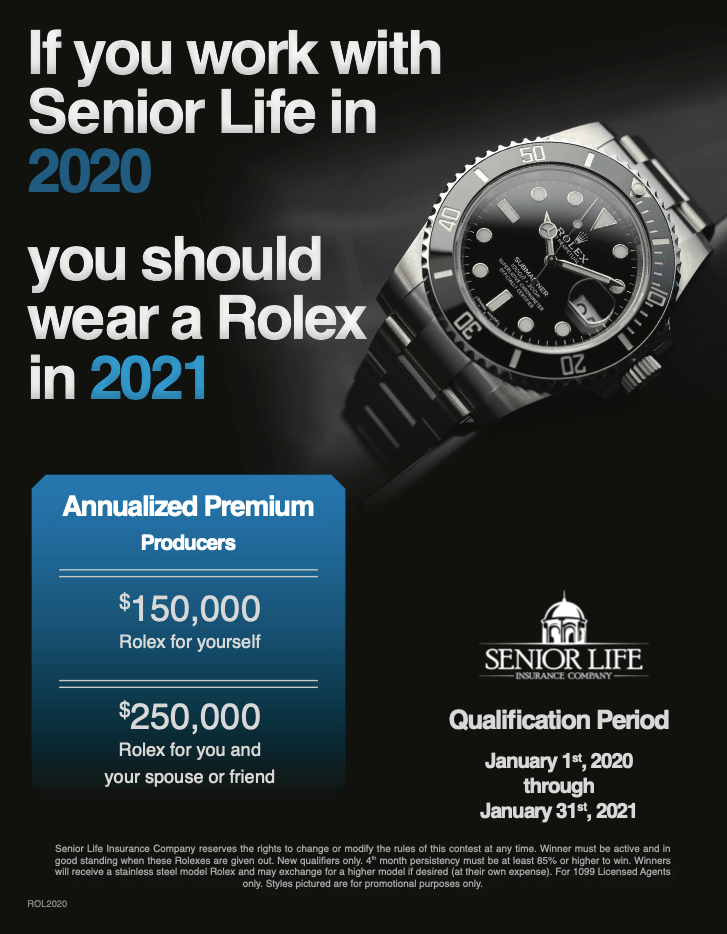

With Senior Life Insurance Company, you have the chance to earn your own Senior Life Insurance Company ring based on your production.

With Senior Life Insurance Company, you have the chance to earn your own Senior Life Insurance Company ring based on your production.